Mapping MENA’s Renewable Energy Supply Chains: The Emergence of Green Energy Ecosystems in the Middle East and North Africa

Introduction

The Middle East and North Africa has the potential to become the world’s largest renewable energy-producing region. Solar energy is MENA’s most abundant renewable energy resource. The Sahara Desert, which covers the majority of North Africa, receives the world’s highest levels of solar irradiation and comprises a territory just slightly smaller than the total area of the United States. The amount of solar energy striking the Sahara Desert is so enormous that, were it all capable of being harnessed for power generation, it would be 7,000 times greater than Europe’s total electricity demand at any given moment.1 Similarly high levels of solar irradiation are also present in the adjacent regions of the Negev Desert, the Jordanian desert, and large swathes of the Arabian Peninsula. MENA’s massive solar energy resources are augmented by ample wind power resources, inland, nearshore, and offshore.

Compared to the immense scale of the resources, renewable energy is virtually untapped in the MENA region. While the Sahara Desert’s solar resources alone theoretically could support an installed power generation capacity of over 1,000,000 gigawatts (GW), the combined installed solar power capacity across the MENA region in 2022 was 16 GW.2 For perspective, the entire MENA region’s installed solar capacity is roughly the same as that of France in 2022,3 a country that relies primarily on nuclear power for its electricity supply, and four times less than Germany’s 67 GW,4 which has shut down its nuclear power plants. The predominance of oil and natural gas production across MENA does not by itself explain the region’s lack of renewable energy power generation capacity. The United States, the world’s leading oil and natural gas producer, boasted 113 GW of installed solar capacity in 2022,5 over five times more than the entire MENA region.6 The statistics for MENA’s wind power capacity are in line with those for solar power.

The comparative paucity of MENA’s renewable energy infrastructure reflects a relatively recent enthusiasm for renewable energy across the region as a whole, with the notable exception of some of the trailblazing nations that form the core focus of this study. From 2012 to 2021, the growth rate in MENA for total installed renewable power generation capacity was 76%, far below the 112% global growth rate for renewable energy.7 During the previous decade, the drive to develop utility-scale renewable energy systems gained political momentum, as several key MENA nations adopted “Vision 2030 plans” with ambitious infrastructure construction initiatives that include massive build-outs of renewable energy infrastructure. As part of these plans and their associated national energy strategies, several MENA countries adopted targets for increasing the role of renewable energy in their respective national energy systems, with the 2030 targets for renewable energy’s share ranging from 15% to 50% of the power supply mix. To meet these targets, many of the proposed projects across the region are scheduled for completion during the current decade.

In mapping the emerging regional trends in renewable energy development and MENA renewable energy supply chains, this study examines the three MENA sub-regions of North Africa, the Arabian Peninsula, and the Levant. While assessing the state of renewable energy across most of the MENA region, the study takes as its primary focus two trailblazing nations in each sub-region: Morocco and Egypt in North Africa; the United Arab Emirates and Saudi Arabia in the Arabian Peninsula; and Jordan and Israel in the Levant. In 2022, Morocco ranked as the most attractive renewable energy market for investment, according to the Renewable Energy Country Attractiveness Index published by international accounting firm EY (Ernst & Young), when normalized for GDP.8 Morocco was also the only MENA country that placed within the top 20 of the RECAI’s “raw” score, ranking 19th and followed by Israel (21), Egypt, (29), and Jordan (38).9 On the Arabian Peninsula, the UAE and Saudi Arabia have positioned themselves at the forefront of rapidly developing renewable energy supply chains.

The most successful MENA nations in developing their renewable energy resources to date are doing so through the establishment of green energy ecosystems, in which the development of utility-scale renewable energy infrastructure is coordinated with that of robust offtake markets and the establishment of commercially viable storage and transportation mechanisms to service them. A critical element for renewable energy development, this study shows that the most robust renewable energy supply chains are emerging from green energy ecosystems. While the importance of electricity interconnection for renewable energy exports will be discussed below, electricity interconnection alone as an offtake mechanism is insufficient to establish robust renewable energy production value chains. These value chains have arisen in the MENA region as a result of the emergence of green energy ecosystems whose offtake markets are anchored in the food-water-energy nexus and the development of green hydrogen production.

Given the challenges across the region in coping with extreme water stress, the MENA countries with the most advanced renewable energy production programs also tend also to be leaders in water desalination. Since agriculture accounts for 80-85% of water consumption across most MENA nations,10 the establishment of green energy ecosystems has emerged through efforts to use renewable energy to ensure the resilience of agri-food production. Beyond desalination, the rise of green hydrogen as a central component of renewable energy production value chains is also anchored in agri-food production, as the source input for fertilizer manufacturing is green ammonia, a green hydrogen derivative.

The attraction of green ammonia initially stemmed from the fact that ammonia, a nitrogen-hydrogen compound, forms the basic component of most synthetic fertilizers upon which modern agri-food production depends. Fertilizer manufacturing accounts for about 70% of global ammonia consumption.11 While the nitrogen is sourced from the air, the hydrogen used for ammonia production is primarily so-called gray hydrogen produced from natural gas in a process that releases considerable quantities of carbon dioxide (CO2), one of the main gasses thought to be responsible for climate change. In contrast to conventional gray hydrogen, green hydrogen is produced by using electricity generated from renewable sources to split water into its hydrogen and oxygen components, creating a versatile, carbon-free (hence, “green”) energy carrier.

Fertilizer industries are incentivizing the development of green ammonia production capacity, as fertilizer producers attempt to ensure their resilience and cost-effectiveness by phasing out natural gas-derived ammonia in favor of climate-smart, supply shock-resistant green hydrogen-derived ammonia produced from renewable energy. Each of the six trailblazing MENA nations analyzed in this study — Morocco, Egypt, the UAE, Saudi Arabia, Jordan, and Israel — is already a significant exporter of fertilizers or fertilizer inputs. With a nearly guaranteed domestic offtake option for fertilizer production, green ammonia has emerged as a preferred end-product of green hydrogen production.

Beyond its use in fertilizer manufacturing, green ammonia is presently the most cost-effective way to store and transport green hydrogen and therefore an important means to transport renewable energy.12 For reasons explained below, green ammonia will likely become the dominant form of traded green hydrogen as opposed to transporting hydrogen gas itself through pipelines. In the form of green ammonia, which can be easily transported by ship, green hydrogen becomes a versatile energy carrier for renewable energy. Being able to transport renewable energy on demand as green ammonia greatly expands the scope of opportunities for developing a diverse array of renewable energy production value chains beyond the limitation of cross-border electricity interconnections.

By recombining green hydrogen and oxygen back into water in a fuel cell, electric current is generated, providing on-demand, climate-smart power. Thus, green ammonia serves as an alternative technology to utility-scale batteries, which require toxic and difficult to obtain minerals, for storing energy produced from renewable sources and then deploying it on demand. While renewable energy exported via electricity interconnection and stored in utility-scale batteries is the rough analogue to the 20th century natural gas trade via pipelines, green ammonia transported on ships is the renewable energy equivalent of liquified natural gas (LNG), which is quickly becoming the dominant form of traded gas.

Given the current state of battery technology development, green ammonia is on track to play a pivotal role in renewable energy supply chains, expanding as well as diversifying the opportunities for developing renewable energy production value chains anchored in the MENA region. The European Union adopted its Hydrogen Strategy for a Climate-Neutral Europe in 2020, formalizing the effort to develop low-carbon hydrogen value chains.13 As discussed below, Germany has been a pioneer in green hydrogen value chain development within the MENA region, having committed €9 billion to its green hydrogen strategy.14 France has also committed €9 billion to developing low-carbon hydrogen value chains,15 while Spain — which seeks to be a supplier to European markets — has committed €18 billion to its hydrogen strategy, doubling its prior anticipated allocation.16

From its foundation in the food-water-energy nexus, green ammonia is emerging as a preferred energy carrier for the greening of industrial manufacturing processes, providing the means by which these processes can be fueled and powered by renewable energy. Beyond fertilizer production, green hydrogen will also increasingly serve as a feedstock fuel in industrial manufacturing, particularly steel production (known as “green steel”) and other metals processing. The worldwide steel sector accounts for about 7% of global CO2 emissions.17 In 2023, Europe’s first green steel production plant, the H2 Green Steel plant, began operation in Sweden with commercial sales expected in 2025.18 This will soon be followed by the EU-funded HYBRIT (Hydrogen Breakthrough Ironmaking Technology) green steel manufacturing facility in Sweden, scheduled to be operational in 2026.19 Beyond Sweden, major green steel production projects are underway across Europe — including in Spain, France, and Germany20 — as well as in South Korea21 and Japan.22 European and Asian green steel production and other green metals processing will expand the exports markets for MENA-produced green hydrogen, encouraging increased foreign investment in renewable energy infrastructure in the region. Concurrently, increased metals demand will spur the expansion of metals production in the MENA region where the green energy is locally produced.

The transition to renewable energy will require additional production of massive quantities of other key metals such as copper, aluminum, and various rare earths for the construction of solar power and wind power infrastructure, as well as the electric cables that will carry the power over long distances. The Energy Transitions Commission has estimated that the energy transition needed to meet 2050 climate targets could require the production of 6.5 billion tons of end use materials — 95% of which would be steel, copper, and aluminum.23 The use of green hydrogen means that renewable energy can power the additional, energy-intensive metals processing required for the construction of new renewable energy production infrastructure. In September 2022, the world’s first low-carbon copper high-voltage direct current (HVDC) power cables were manufactured in Sweden.24 HVDC cables are used in undersea electricity interconnectors that provide MENA power producers the means to export their electricity beyond the region. Major undersea interconnection projects are under way in Morocco, Tunisia, Egypt, and Israel, and are likely imminent in the UAE and Saudi Arabia. Similarly, high-voltage alternating current power cables used in transmission lines are composed primarily of aluminum. As discussed below, the UAE has already pioneered the production of green aluminum from solar power. This green circular economy dynamic is likely to spur more local mining and metals processing in the MENA region where the renewable energy is produced. Four of the six trailblazing nations in this study — Morocco, Egypt, the UAE, and Saudi Arabia — already have significant mining and metal processing sectors. In the case of Morocco and Saudi Arabia in particular, these sectors are in a process of rapid expansion, with Egypt attempting to follow suit. The growth of mining and metals processing in these countries will incentivize further renewable energy power generation development in a mutually reinforcing process.

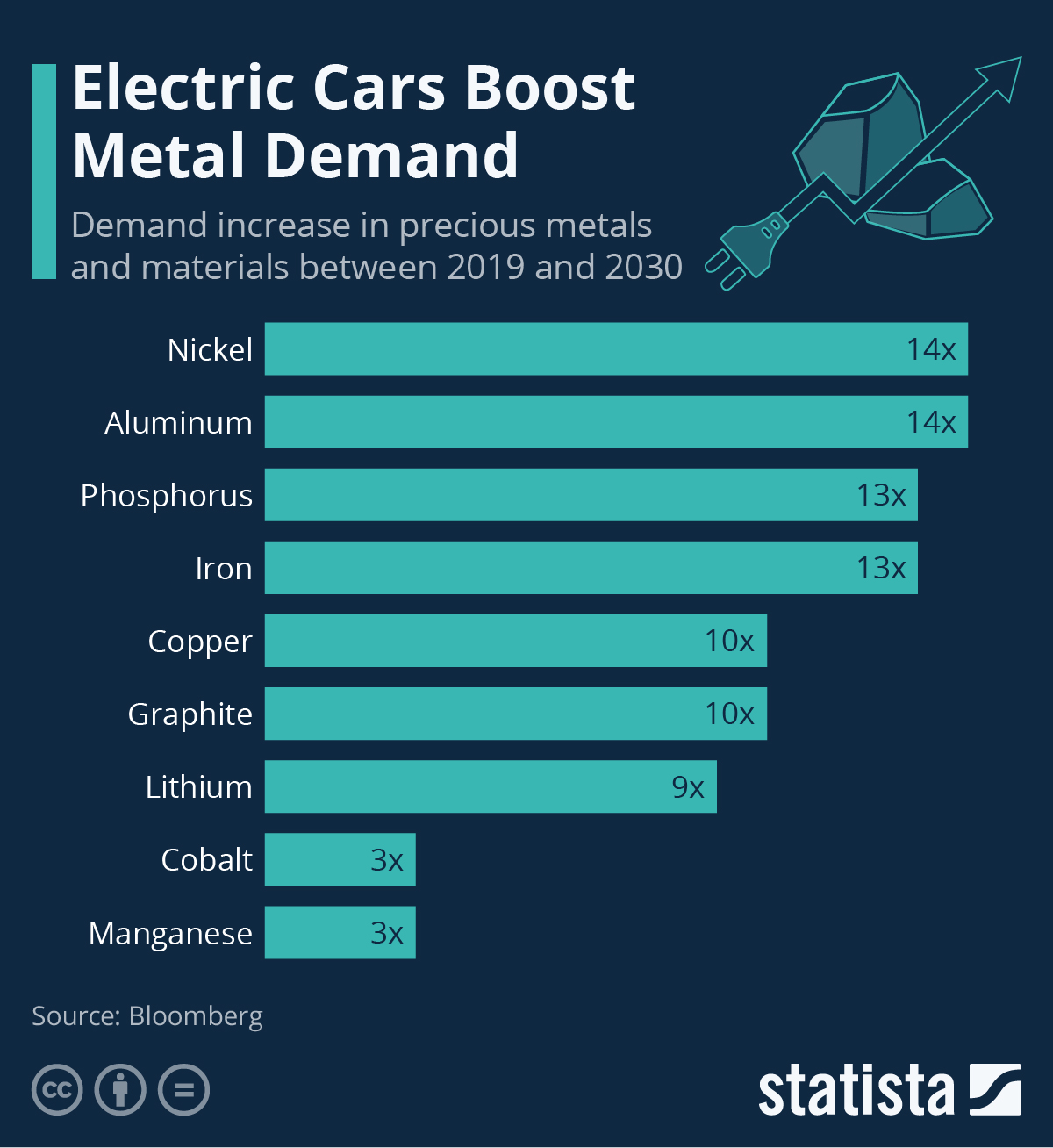

Green metals production powered by renewable energy also comprises a vital part of the green energy ecosystem through its intimate relationship with green mobility — the transition to the production and widespread use of electric vehicles (EVs) and their charging infrastructure. According to a Bloomberg forecast of EV metals, aluminum and nickel demand will experience a fourteenfold increase by 2030, while phosphorous and iron demand will increase ten times in the same period.26 A tenfold demand increase is expected for copper and graphite, while lithium demand will increase ninefold.27 Morocco, which has a well-developed automotive manufacturing sector, has already started large-scale EV production and expects to be producing 250,000 electric cars by 2025.28 Morocco also has a rapidly developing EV battery production sector and is becoming a global center for EV battery metal recycling. Each of the manufacturing processes associated with green mobility could be powered by renewable energy, creating green circular production.

Green mobility, beyond Morocco, is increasingly becoming an important component of MENA green energy ecosystems. In 2023, both the UAE and Saudi Arabia initiated an EV manufacturing sector. Egypt has also been eyeing the development of EV production. The UAE has opened a recycling facility for end-of-life EV batteries as well. The main customers for the UAE’s green aluminum are European automakers. MENA renewable energy will power the metals and materials manufacturing, either locally or outside the region, for the components of climate-smart cars, trucks, busses, and aircraft. With their already existing infrastructure for fossil fuels and petrochemical production, some Gulf states are also at the forefront of developing sustainable aviation fuel from green hydrogen.

Although European firms have been leading efforts to partner with MENA nations to develop their green hydrogen potential, Asian markets may rapidly develop if the coal-burning regions of Asia move toward “co-firing,” using both ammonia and coal as fuel in hitherto coal-fired power plants.29 Japan has been pioneering the development of co-firing technology and, in 2023, successfully tested the operation of one its major coal plants using a fuel mix of 20% ammonia and 80% coal.30 Tokyo aims to achieve 50-50 fuel during the 2030s and then phase out coal entirely in favor of 100% ammonia-fired plants by the 2050s.31 To meet their own commitments to achieve carbon-neutrality, Japan and other Asian nations using co-firing as an intermediate step will likely seek to import MENA-produced green ammonia, adding a further dimension to MENA renewable energy supply chains and their green energy ecosystems.

In examining the state of renewable energy development across the MENA region and renewable energy supply chains, the formation of green energy ecosystems is the primary indicator for success and growth. Thus, using the state of a MENA nation’s green energy ecosystem as an analytical metric provides an insightful means to understand and evaluate the renewable energy power generation mega-project initiatives in that nation. While countries will differ in their pathways to developing a green energy ecosystem, this study suggests that initiatives for renewable energy development succeed when they participate in green energy ecosystems while those that remain primarily on the drawing board are the ones unconnected to such an ecosystem. Green energy ecosystems become a marker for the robustness for renewable energy value chains within MENA and between the MENA region and markets in Europe, Asia, and Sub-Saharan Africa. The green energy ecosystems further constitute an important factor for understanding the prospects of cooperation within the three sub-regions of the Middle East and North Africa. This is a particular concern for the Levant region, where the lack of available land for utility-scale renewable energy will require more regional cooperation. The state of green energy ecosystems will further shape the patterns of cooperation among the MENA sub-regions of North Africa, the Arabian Peninsula, and the Levant.

North Africa

The nations of North Africa are awash in abundant solar energy resources. From Morocco to Egypt, large swathes of the region boast the world's largest photovoltaic (PV) power and concentrated solar power (CSP) potential,32 as direct normal irradiation (DNI) levels reach or exceed 2,300 kilowatt hours per square meter.33 By comparison, the most sun-soaked areas of southern Germany — one of MENA’s main renewable energy partners — reach only half that DNI level, with most of the country receiving even less solar irradiation.34 The high DNI region of North Africa includes the Sahara Desert — comprising 9 million square kilometers, over twice the total area of the EU. In addition to receiving the world’s highest levels of solar irradiation, the Sahara Desert possesses an abundance of the open land necessary to host the distributed infrastructure required by solar power generation. Even converting only one-thousandth of the solar energy that hits the Sahara into usable power would provide enough electricity to entirely power Europe at any given moment as well as to supply the current power demand of the entire African continent several times over.35 In short, North Africa has sufficient solar energy resources to export energy while powering its own industrial and agricultural development. Additionally, North Africa has ample onshore wind power resources, as well as offshore wind resources from Morocco’s Atlantic coast to Egypt’s Gulf of Suez that complement its solar resources.36 In regions where there are reliably constant night-time winds, solar and wind power may be combined to provide 24-hour baseload power, as is the goal of the Morocco-to-UK Xlinks interconnector project, discussed below.

The attraction of harnessing North Africa’s vast renewable energy resources for electricity exports gave rise to the ambitious Desertec project initiated in Germany in 2009. The forward-looking project sought to create solar and wind power facilities across a 6,500 square mile area of North Africa, along with the requisite trans-Mediterranean electricity interconnection to supply about 15% of Europe’s electricity demand. Visionary but poorly conceived, the ill-fated Desertec project collapsed in 2014.37 Although the private sector played a role through public-private partnerships, Desertec evolved out of a development aid framework and was not sufficiently attuned to North Africa’s economic and political needs. Consequently, the project also elicited concerns that it was laying the foundations for green energy neo-colonialism. Desertec’s demise dampened enthusiasm for renewable energy transmission via trans-Mediterranean undersea electric cables, casting doubts on its commercial feasibility.

Despite the setback, Morocco and Egypt continued with their plans to construct large, utility-scale solar and wind power facilities. And while both countries are engaged in the construction of undersea electricity interconnectors to Europe, Morocco and Egypt’s advances in the construction of renewable energy systems have laid the foundation for these nations to also become North Africa’s trailblazers in the development of green hydrogen as an alternative carrier for renewable energy.

The green ammonia production has contributed to the development of a robust green energy ecosystem in Morocco and to a lesser extent in Egypt as well. With no significant reserves of fossil fuels, Morocco’s dependence on imported natural gas and coal for industrial and residential power has provided a strong economic motivation to replace their use with renewable energy and green hydrogen. Egypt, by contrast, is Africa’s second largest natural gas producer, with an annual output of about 65 billion cubic meters (bcm) prior to the 2023 financial crisis.38 Contrary to the assumption that investments in natural gas compete with renewable energy investments in a zero-sum game, Egypt has developed its natural gas and renewable energy resources in tandem. Cairo’s efforts to develop natural gas self-sufficiency spurred it to concurrently advance the development of renewable energy power generation infrastructure, developing over 2 GW of combined solar and wind capacity. Although Morocco and Egypt stand as exemplars of two different paradigms for the development of green energy in the MENA region — non-hydrocarbon industry-based economies versus heavily hydrocarbon-based economies — these distinct exemplars share a common pathway for the initiation of green energy ecosystems: both countries have highly developed fertilizer manufacturing sectors that have incentivized green hydrogen development.

Morocco: Developing Renewable Energy Supply Chains through a Green Energy Ecosystem

Morocco has been a pioneer in renewable energy development in the MENA region by establishing a dynamic green energy ecosystem anchored in the food-water-energy nexus. Reflecting a holistic strategic vision, the four key state pillars of Morocco’s efforts are managed under the Ministry of Energy Transition and Sustainable Development (formerly the Ministry of Energy, Mines, and the Environment) and include the Morocco Agency for Sustainable Energy (MASEN); the Institute for Research for Solar Energy and New Energies (IRESEN); the National Office of Electricity and Potable Water (ONEE); and the OCP Group (originally, Office Chérifien des Phosphates), the world’s largest producer of phosphate products and fourth largest exporter of fertilizer. Morocco possesses over 73% of the world’s phosphate rock reserves from which the phosphorus used in these fertilizers is derived.39 Prior to the 2021 natural gas price shocks, OCP’s total revenue in 2020 amounted to $5.94 billion,40 accounting for about 20% of the kingdom’s export revenues.41 OCP’s massive phosphate mining and fertilizer manufacturing sector has transformed Morocco into a gatekeeper of the world’s food supply,42 making the sustainability of the industry through energy transition a matter of national interest for Morocco as well as the nations that depend on its exports.

OCP covers 89% of the energy needs for its phosphate and phosphorus fertilizer production through co-generation (reusing exhaust energy to create cleaner and cheaper power from fossil fuels) and renewable sources and heading toward covering 100% of its energy needs in this manner.43 To ensure its transition beyond fossil fuels, OCP established OCP Green Energy SA in 2022, as a wholly owned subsidiary to develop its renewable energy generation activities, committing an investment of $13 billion during the 2023-27 period.44 Dedicated solar plants are being built in the mining towns of Benguerir and Khouribga, home to Morocco's largest phosphate reserves, as well as in other locations.

With the exception of OCP, which was reorganized in 2008, the state institutional framework for Morocco’s green energy ecosystem was initiated in 2010 with the creation of MASEN as a private company with public funding to oversee the development of Morocco’s massive, muti-phase Noor solar energy power generation project. The president of MASEN previously served as the head of Caisse de Dépot et de Gestion (CDG), which manages long-terms savings and invests in Morocco’s infrastructure development.45 MASEN’s board includes the minister of economy and finance, the managing director of ONEE, the administrator of the Ministry of Energy Transition and Sustainable Development, and the administrator of the Ministry of Industry, Trade, Investment, Green, and Digital Economy.46

IRESEN was created in 2011as the research arm of Morocco’s national energy program across the entire spectrum of the value chains within the green energy ecosystem, including solar energy systems, green hydrogen systems, and electric mobility.47 IRESEN oversees a network of green energy research and innovation platforms and funds for applied research and collaborative innovation projects, helping to propel Morocco toward the forefront of next-generation green energy technology development.48 IRESEN’s board includes members from the Ministry of Energy Transition and Sustainable Development, MASEN, ONEE, and OCP as well as several other key state institutions, including the mining sector’s National Office of Hydrocarbons and Mines and Morocco’s state-owned mining company Managem.49 Following IRESEN, ONEE was formed in 2012 through the integration of the National Office of Electricity (created in 1963) and the National Office of Drinking Water (created in 1972), reflecting Morocco’s ambition to manage its energy system to provide sufficient water for human consumption as well as its growing industrial and especially agricultural sectors.

According to the Ministry of Energy Transition and Sustainable Development, renewable energy accounted for 38% of Morocco’s 2022 installed power generation capacity, with the largest proportion being generated by hydroelectric power.50 In 2022, Morocco’s installed capacity from wind power stood at 1.77 GW while solar power stood at 1.43 GW, representing respectively 14.38% and 7.82% of Morocco’s total installed capacity of 4.031 GW. Due to the kingdom’s progress toward its 2020 energy transition target of having 42% of installed capacity come from renewables, Rabat accelerated its energy transition program by setting a revised 2030 target of renewables accounting for 52% of total installed capacity, with the increase coming mostly from the construction of additional solar and wind power infrastructure. Between 2023 and 2027, Morocco is slated to add approximately 6.5 GW of renewable power generation capacity at a cost of $5.6 billion.51

Morocco’s ongoing solar power development program consists of a cluster of “Noor” solar power projects spread across the country.52 The current flagship projects are Noor I, II, and III with a combined installed capacity of 1.6 GW. Noor I, also known Ouarzazate Solar Power Station, features the world’s largest CSP facility with a 580 megawatt (MW) installed capacity developed in four phases with PV infrastructure for a total of 800 MW.53 Noor II and Noor III, also known as Noor Midelt II and Noor Midelt III, are each in the process of developing a 400 MW installed capacity of PV solar power.54 MASEN prequalified companies for the Midelt II and III projects in July and August 2023, respectively.55 Several of the smaller solar projects across the kingdom were or are being developed by ONEE.56

Morocco’s wind power installed capacity is distributed over nine projects across the country with over two-thirds located in coastal regions.57 Newer and larger wind power development projects are directly driven by the needs of Morocco’s green energy ecosystem and international renewable energy supply chains. For example, Morocco’s largest wind power facility is being developed by Total Eren, now a wholly owned subsidiary of French energy giant TotalEnergies,58 as part of the company’s larger $10 billion project to establish green ammonia production in Morocco’s Guelmim-Oued Nour region.59 The 5 GW wind farm will be combined with 5 GW of dedicated solar capacity to power the green ammonia plant, taking advantage of the region’s near constant nighttime winds to provide virtually 24-7 renewable power.60

Morocco’s green energy ecosystem is anchored in the food-water-energy nexus through its agri-food production and fertilizer manufacturing industries. The country’s renewable energy program evolved in tandem with the implementation of its 2010-2020 Green Morocco Plan (Plan Maroc Vert, PMV) to expand its high-value agricultural export sector, which has resulted in Morocco's agri-food sector now accounting for 21% of its exports.61 The PMV’s successor plan, the 10-year Green Generation 2020-2030 initiative, is focused on enhancing the resilience and sustainability of the country's agricultural production through the expanded production and use of renewable energy.62 To ensure sufficient water for agriculture as well as human consumption in the face of increasing water stress due to climate change, Morocco adopted a $40 billion National Water Plan 2020-2050 that includes the construction of more desalination plants.63 Seawater desalination is highly energy intensive, typically requiring 10 times the amount of energy to produce the same volume of water as conventional surface water treatment.64 Morocco’s additional desalination plants will ultimately require new power generation capacity from renewable energy sources or possibly nuclear power.65

The creation of fertilizer manufacturing value chains using renewable energy and green hydrogen is essential for the establishment of sustainable and resilient food production value chains worldwide. One of the highest priorities in this domain is transitioning fertilizer production from using ammonia synthesized from natural gas-derived gray hydrogen to ammonia produced from green hydrogen. The majority of green hydrogen's production costs, about 70%, come from the electricity required to split water into its hydrogen and oxygen components and could be powered by Morocco's solar energy and wind energy resources.

Morocco’s rise as a global leader in green hydrogen was prompted by its objective of using its derivative green ammonia to supply the kingdom’s lucrative fertilizer industry. The country’s lack of natural gas places a limiting factor on the resilience of its fertilizer production, which requires ammonia, now produced from natural gas-derived gray hydrogen. Prior to the outbreak of the war in Ukraine in 2022, OCP needed to import 1.5 to 2 million tons of ammonia per year to meet its production.66 Since the war, OCP is eyeing a 58% increase in its production capacity to fill European and global fertilizer supply shortfalls.67

To create sustainable and resilient production for exports, Morocco will ultimately need to replace its imported ammonia made from gray hydrogen with green ammonia produced locally powered by its solar and wind energy resources. Morocco began its development of green hydrogen production in partnership with Germany in 2018 when OCP signed a cooperation agreement with Germany’s Fraunhofer Institute to develop a pilot green hydrogen manufacturing project in cooperation with IRESEN.68 Replicating the institute's pilot plant in Germany, the Moroccan pilot was slated to have an annual production capacity of 1,460 tons of green ammonia.69 When Berlin announced its German National Hydrogen Strategy in June 2020,70 Morocco became the first country to sign a green hydrogen agreement with Berlin to create industrial-scale green hydrogen production.71 Using Morocco's renewable power infrastructure, the project was financed by the German development bank KfW and managed by MASEN.72 The two projects have been conducted within a development aid framework and faced political setbacks over Berlin’s posture concerning Morocco’s autonomy plan for the Sahara region until Germany’s 2022 political reconciliation with Rabat.73

In the wake of these events and in light of the rising demand for ammonia, Morocco has advanced multiple private sector development projects backed by Portugal, the Netherlands, Italy, and the EU.74 Morocco's largest green ammonia project under development is the Irish-Portuguese HEVO facility, which is slated to have an initial annual capacity of 183,000 tons by 2026, equivalent to approximately 10% of OCP's production input requirements.75 Rabat signed a memorandum of understanding (MoU) with Dutch oil trading giant Vitol to market the green ammonia in Europe.76

The Netherlands, the world’s second largest food exporter and the EU’s largest fertilizer user per hectare, itself provided loan guarantees in 2022 for the Dutch green hydrogen firm Proton Ventures to build a green ammonia plant at Morocco’s Jorf Lasfar port.77 The Dutch pilot green ammonia plant will have an annual production capacity of 1,460 tons,78 the same as the first stalled German project. Also in 2022, the Dutch state-owned natural gas transmission network operator Gasunie, the Netherlands-headquartered bulk handling giant HES International, and the Dutch global leader in tank storage Vopak formed a consortium for the construction of a new green ammonia import terminal at Rotterdam’s Maasvlakte port.79 The terminal is intended to handle green ammonia imports to Europe and is expected to be operational by 2026. Further signs of Europe’s eagerness to import Moroccan green hydrogen are the previously discussed green ammonia project in Guelmim-Oued Nour region being developed by Total Eren and an MoU signed by Saipem (controlled by Italian energy major Eni) and Italy-based Alboran Hydrogen to build a green ammonia plant in Morocco.80

For its part, OCP made public its plans in June 2023 to construct its own $7 billion green ammonia plant to help the company replace its annual import of $2 billion of gray ammonia with domestically produced green ammonia, expecting to have an initial annual production capacity of 200,000 tons by 2026.81 The world’s fourth largest fertilizer exporter is aiming to raise its own green ammonia production to 1 million tons by 2027 and reach 3 million tons by 2032. Thus, with the completion of the projects currently under consideration, Morocco could export over 1-3 million tons annually.82 In addition to fertilizer production, the green ammonia can also be exported to Europe, and possibly more distant East Asia, for industrial manufacturing processes and as fuel ammonia.

Green mobility, in the form of EV manufacturing, constitutes the other major industrial pillar of Morocco’s green energy ecosystem. Morocco’s impressive automotive industry now accounts for about 25% of the kingdom’s GDP and employs one-quarter of a million Moroccans.83 The largest automaker in Africa, Morocco’s annual production capacity is over 700,000 vehicles per year and is on its way to producing 1 million or more vehicles by 2025,84 at least 250,000 of which will be EVs.85 European automakers Groupe Renault and Groupe PSA (now part of the Stellantis conglomerate) operate manufacturing plants in the kingdom that are supplied by 250 international firms from the United States, Europe, Japan, China, and elsewhere, each with their own local plants to supply automotive components. As a consequence, Europe’s two best-selling car models — the Peugeot 208 and Renault’s Dacia Sandero — are made in Morocco.86 Now, Rabat has its sights on manufacturing their EV versions,87 while Germany’s Opel and Italy’s Fiat have already begun producing EV models in Morocco.88

The key to Morocco’s rise as a green mobility manufacturing giant will be expanding its automotive ecosystem to include local manufacture of lithium ion (Li-ion) batteries, which represent 30% to 40% of the cost of the average EV.89 The urgency for Morocco is compounded by the fact that Europe is likely to be one of the centers of immediate EV growth, spurred by the European Commission’s July 2021 directive to phase out all fossil fuel-powered vehicles in the EU by 2035.90 Morocco cannot afford to lose its European market, which accounts for 90% of its exports.91 Morocco’s renewable energy also provides a competitive advantage as automakers like Renault have set carbon reduction goals for its EV batteries of 20% by 2025 and 35% by 2030, compared to 2020 levels.92 Morocco can further reduce its carbon footprint through recycling of end-of-life batteries. In 2022, global mining and metal trading giant Glencore entered into a partnership with Managem to produce recycled cobalt from disused Li-ion batteries at Managem’s hydrometallurgical refining facilities operated by its subsidiary Compagnie de Tifnout Tighanimine (CCT).93 Glencore will provide CCT with so-called black mass, processed from dismantled and shredded Li-ion batteries. In addition to cobalt, the partnership is also seeking to extract lithium carbonate and nickel hydroxide from the black mass. If extracted in sufficient quantities, Morocco could locally source all of the major metals used in nickel manganese cobalt (NMC) Li-ion batteries and with a low carbon footprint if the processes are powered with renewable energy.

Morocco’s massive phosphate reserves are a critical factor in its transformation into a green global-scale EV battery production hub. A growing trend in electric passenger cars is to replace NMC Li-ion batteries with lithium iron phosphate (LFP) batteries, substituting expensive cobalt and nickel as well as manganese for relatively cheaper phosphate and iron.94 The increasing utilization of LFP batteries favors Morocco for EV battery production as the country is the world’s second largest phosphate producer, after China.95 Morocco is also a net exporter of iron ore.96 By manufacturing LFP batteries for EVs instead of their NMC counterparts, Morocco would enjoy a cost advantage of upward of 70% per kilogram.97 Since 2023, five Chinese EV battery manufacturers have made substantial investments in local EV battery production plants and battery metals recycling facilities, cementing Morocco’s position in the EV battery supply chain. If these EV battery recycling ventures are powered with renewable energy, the country could further reduce the carbon footprint of its LFP batteries to achieve a significant market advantage.98 Morocco will need to expand its phosphate and phosphoric acid production to make LFP EV batteries, especially to avoid demand pressure competition from fertilizer production. OCP’s additional output of phosphates and phosphoric acid will need to be powered by renewable energy sources, creating green circular production for the battery component of EV manufacturing.

Morocco’s electricity interconnections to Europe also play an important role in renewable energy development and the establishment of renewable energy supply chains. The most prominent example is the ambitious Morocco-to-UK Xlinks interconnector, which involves the construction of 11.5 GW of dedicated renewable power. The $20 billion project is developing 8 GW of solar power and 3.5 GW of wind power in the Guelmim-Oued Nour region that will supply the UK with electricity for more than 19 hours per day via a 3.6 GW interconnector between the two countries.99 The two 1.8 GW undersea cables will need to traverse the formidable distance of 3,800 kilometers, but will supply about 8% of the UK’s power demand. Despite the technological challenges, the Xlinks project is expected to be completed in 2030.100

Morocco already has two interconnections with Spain with a total exchange capacity of 800 MW; a third interconnector of 700 MW is now under development and is expected to be operational in 2026.101 In December 2023, Morocco and Portugal signed a joint declaration to advance the feasibility studies for the establishment of an electricity connector between the two countries.102 However, the Iberian Peninsula is a relatively isolated island in the EU electricity grid, as Spain's 2020 exchange with the EU system’s was only 3% of its installed capacity, far below the EU minimum standard of 10% (which has since been raised to 15%).103 Morocco’s interconnections with Spain and Portugal are unlikely to provide sufficient access to the wider EU electricity market to spur investments in additional renewable energy infrastructure or to establish renewable energy supply chains. The political tensions between Morocco and Algeria further make it unlikely that the former could access the EU electricity market via trans-Mediterranean interconnection from the central Maghreb. Morocco’s international renewable energy supply chains will be based primarily on green hydrogen as well as phosphates, minerals and metals, fertilizers, agri-food products, and EVs whose production was powered, in part or entirely, with renewable energy resources.

Egypt: Recharging Progress by Developing Diversified Renewable Energy Supply Chains

After almost a decade of considerable progress, Egypt’s renewable energy development is at a crossroads. Egypt’s 2035 Integrated Sustainable Energy Strategy aims to boost power production from renewable sources to 10 times the current level to comprise 42% of Egypt's installed power generation capacity by 2035.104 Cairo’s ambitious 2019 energy policy calls for 61 GW of installed capacity from renewables, of which 32 GW would be from PV solar power, 12 GW from CSP, and 18 GW from wind power. The plan was formulated after a successful five-year period of developing Egypt’s energy infrastructure. The country’s economic crisis, with its high inflation rate, shrinking foreign reserves, and crippling cost of debt servicing, has cast doubt on its ability to meet these targets. Nevertheless, the foundations that were established remain and still can be utilized to great effect. Egypt’s development of a green energy ecosystem that more deliberately connects renewable energy production to a diversity of dedicated offtake mechanisms could help provide it with a path out of its current economic impasse.

With the discovery of the Zohr offshore natural gas field in 2015, the Mediterranean’s largest find to date, Egypt devoted considerable resources to developing its natural gas sector and gas-fired power plants to ensure the country’s energy security. In 2019, thanks to production from its large offshore natural gas deposits, Egypt achieved natural gas self-sufficiency and became a net energy exporter in the form of LNG. At the same time as it developed and installed the gas-fired power plants, Cairo also oversaw the construction of Egypt’s flagship renewable power project — the massive Benban PV solar park outside of Aswan.105 The $4 billion solar complex has an installed capacity of 1.8 GW.106 Egypt also built two wind power projects, the 580 MW Gabel el-Zait wind farm near Ras Ghareb (the country’s largest, completed in 2018) and the onshore coastal 262.5 MW Gulf of Suez I wind farm (completed in 2019), with the 545 MW Zafarana wind farm having been completed much earlier in 2010.107 By developing natural gas in conjunction with renewables, Egypt had reversed its 6 GW electricity generation capacity deficit into a surplus of 15 GW between 2016 and 2022.108

To cope with the 2023 economic crisis, the government reintroduced rolling power cuts in Egypt so that the natural gas not used for domestic power generation could be sold as LNG exports, bringing $300 million per month into the cash-strapped state coffers but eliminating Egypt’s electricity surplus.109 Natural gas supplies to Egypt’s fertilizer sector were reportedly cut by 30%.110 The situation is exacerbated by an annual deficit of 30-35 billion cubic meters of water, equivalent to about 60% of what the Nile River contributes to Egypt’s water supply.111 The water deficit is a main contributor to the country’s need for food imports, which requires the government to go further into debt by spending precious foreign reserves to purchase imported food and then subsidizing it to make it affordable for Egypt’s citizens.112 To address the problem, Egypt has adopted the National Water Resources Plan 2017-2037 whose large-scale infrastructure program would cost $50 billion, including the building of 21 desalination plants at a cost of $8 billion.113 These plants will need to be powered by electricity generated from either additional hydrocarbon or renewable energy resources.

Egypt’s current dilemma shows that offtake for renewable energy by electricity interconnection alone is insufficient for sustained green energy development. Renewable energy also needs to be dedicated to high-value-added production for foreign export revenues or production for domestic consumption that would reduce the need for expensive imports (such as the use of renewable powered water desalination and fertilizer production to support the production of staple food crops). Green industrial manufacturing and agrifood production are necessary components of a green energy ecosystem to ensure the resilience and expansion of renewable energy production. Green hydrogen in the form of green ammonia constitutes a versatile energy carrier that could allow Egypt to achieve both value-added export revenues and import replacement.

Egypt’s nascent green hydrogen industry, as in the case of Morocco, is primarily focused on green ammonia. Before the 2023 economic crisis, Egypt was the world's seventh largest ammonia producer, just behind Saudi Arabia, the leading Middle Eastern producer.114 Already a major gray ammonia producer, Egypt can utilize its existing ammonia storage and transportation infrastructure for green ammonia. As such, green ammonia is likely to form a central part of Egypt's low carbon hydrogen strategy for both domestic use and exports. In addition to helping Cairo reach its 2035 energy transition goals, reducing the amount of natural gas required for domestic ammonia production will also free up supplies to be sold as LNG.

In 2021, Cairo had already set into motion a few initial green hydrogen projects that led to a spate of additional proposals. The Egyptian Electricity Holding Company (EEHC) signed an MoU in August 2021 with Siemens, which built the country's gas power plants, to jointly develop a hydrogen-based industry in Egypt with export capabilities, intended to maximize hydrogen production based on renewable energy sources.115 In 2021, Egypt also signed an agreement with the Belgian conglomerate DEME to conduct feasibility studies for the production and export of green hydrogen.116 Already involved in coastal land reclamation for Egypt's Mediterranean port capacity expansion, DEME will reportedly help to determine the optimal locations for hydrogen production hubs.117 Locating Egypt's green hydrogen facilities is a critical task. The country’s estimated 2019 “gray” hydrogen production totaled 1.82 million tons.118 To produce this amount as green hydrogen would require approximately 16.22 million cubic meters (mcm) of water. Although water consumption accounts for only a small share of the total cost of green hydrogen production, the supply of water as an input is a critical issue in water-scarce Egypt. Given average annual rainfall of only 33.3 mm and a lack of permanent surface water across large swaths of the country,119 coastal green hydrogen production sites with dedicated water desalination units also powered by renewable energy are a necessity.

In July 2021, Italian energy major Eni, one of Egypt's natural gas partners and the lead operator of the Zohr field, signed an agreement with EEHC to assess the technical and commercial feasibility of producing both green hydrogen and blue hydrogen.120 For the latter, Eni is eyeing the possibility of using Egypt's depleted natural gas fields for the storage of CO2 produced by carbon capture. The country is currently the world's sixth largest producer of urea, also used in nitrogen-based fertilizers, and could relatively easily use the captured CO2 for urea manufacture.121

One of Egypt's most promising early green hydrogen projects will be constructed on the western shore of the Gulf of Suez. The Norwegian renewable energy company Scatec and Dutch-Emirati fertilizer producer Fertiglobe, in partnership with the Sovereign Fund of Egypt, are building a green hydrogen facility in the industrial zone of the Red Sea port of Ain Sokhna, near Fertiglobe's subsidiary Egypt Basic Industries Corporation (EBIC).122 Scatec will build and operate the facility with Fertiglobe enjoying a long-term offtake agreement for its green hydrogen output as a feedstock for EBIC's green ammonia production.123

For Egypt to replace its entire gray hydrogen production with domestically produced green hydrogen, the country would need an estimated 21 GW of electrolyzer capacity,124 making Cairo likely to opt for a combination of green and blue hydrogen as it seeks to capture market share in European and Asian markets. Ultimately, Cairo aims to capture 5-8% of the global market for green hydrogen, as the value of the clean hydrogen market is expected to surpass that of the LNG trade by 2030 and continue to grow to $1.4 trillion by 2050.125

In October 2022, in the run-up to Egypt’s hosting of the United Nations Climate Change Conference (27th Conference of the Parties, COP27) in November 2022, the European Bank for Reconstruction and Development granted Egypt an equity bridge loan of up to $80 million for developing its green hydrogen production infrastructure.126 At COP27, Egypt’s minister of energy announced an outline for the country’s national clean hydrogen strategy and signed framework agreements with Fortescue Future Industries (the green energy arm of Australian metals giant Fortescue), India’s ReNew Power, Dubai-based AMEA Power, Saudi project developer Alfanar, the London-headquartered, Africa-focused green energy developer Globeleq, Total Energies, EDF, and Scatec.127 Most of the agreements concerned project development around the Ain Sokhna port and the Suez Canal Economic Zone (SCZone), with some building upon pre-existing projects. Energy China signed an MoU to invest approximately $7 billion in the SCZone as well.128

Also on the sidelines of COP27, a Masdar-led consortium with Emirati-Egyptian joint venture Infinity Power and Egypt’s Hassan Allam Utilities signed a framework agreement for the construction of a 2 GW green hydrogen facility in the SCZone, set to be operational in 2026.129 The framework agreement, signed with NREA, EETC, and the Sovereign Fund of Egypt, follows two April 2022 MoUs inked by Egypt with the Masdar-led consortium to construct two green hydrogen facilities with a combined electrolyzer capacity of 4 GW. The other green hydrogen facility is to be built on Egypt’s Mediterranean coast, with the 2030 target of a combined annual green hydrogen output from both facilities of 480,000 tons.130 The week prior, the same consortium of Masdar, Infinity Power, and Hassan Allan Utilities signed an agreement for the development of 10 GW wind project, potentially saving about $5 billion in natural gas costs per year.131 The electric output would also be sufficient to power the green hydrogen production facilities while providing electricity for other industrial or residential power needs.

The collaboration between Masdar and Infinity Power, along with its Egyptian partners reflects Cairo and Abu Dhabi’s mutual interest in Egypt’s emergence as a regional hub for green hydrogen exports to both European and Asian markets.132 Speaking at the signing ceremony for the framework agreement for the SCZone green hydrogen plant, Infinity Power’s chairman said the project would “help position Egypt as a Green Fuel Hub, propelling the country forward on its journey in becoming a green economy.”133

In August 2023, Egypt established a National Council for Green Hydrogen and its Derivatives to monitor the implementation of its National Green Hydrogen Strategy and ensure its regional and international competitiveness in the sector, particularly in overcoming obstacles to attracting investment.134 Subsequently, Egypt’s minister of electricity announced that Cairo’s goal was to capture 5-8% of the global commercial market for green hydrogen,135 while the minister of finance announced that it would offer tax incentives ranging from 33% to 55% and use other financing mechanisms to encourage green hydrogen investment.136

China’s push to develop a manufacturing base in Egypt through the appliance manufacturing sector may also open possibilities for Cairo to develop a more diversified green energy ecosystem via green hydrogen or dedicated renewable power infrastructure. In 2023, Chinese home appliance giant Haier completed the first phase of its factory build-out in Egypt and it plans to start production of air conditioners, washing machines, and televisions in 2024. With the additional of refrigerators and freezers, Haier expects to produce 1 million home appliances per year in Egypt.137 Chinese firms are also beginning to develop a manufacturing base for industrial products that could serve as inputs, such as iron, steel, and chemicals, all of which could possibly be powered with green hydrogen.

Electricity interconnection remains a potential mechanism for Egypt to establish renewable energy supply chains, and the progress in advancing proposals for Egypt’s trans-Mediterranean interconnection with Europe as well as the expanded interconnections constructed with Saudi Arabia and Sudan should not be overlooked. Egypt could access wider EU markets via the proposed 2 GW Euro-Africa interconnector to transport electricity from Egypt to Europe via Cyprus and Greece or the proposed 3 GW direct Greece-Egypt (GREGY) interconnector.138 The soon-to-be operational $1.6 billion, 3 GW interconnection between Egypt and Saudi Arabia could be used to bolster electricity exports to Europe through Saudi contributions.139 The planned expansion of Egypt’s interconnection with Jordan from 300 MW to 2 GW could also enable Egyptian electricity exports to the kingdom, bolstering Jordan’s own exports to Lebanon, Syria, and Iraq (see discussion below).140

Egypt has made significant upgrades to its electricity interconnections with Africa as well. In December 2019, Egypt announced that it was prepared to export 20% of its surplus electricity to African nations.141 Sudan, Egypt’s neighbor to the south, has a 60% rate of access to electricity.142 Egypt and Sudan’s grid connection became operational in April 2020, and will reach 300 MW upon completion.143 Egypt could theoretically export electricity to other neighboring countries facing power shortages, like Chad.

Despite Egypt’s progress in establishing interconnections on three continents, Egypt must first return to generating electricity surpluses before it can export significant amounts of power. Under these circumstances, renewable energy supply chains via interconnection are unlikely to materialize soon unless the interconnections are accompanied by dedicated renewable power infrastructure.

Sudan: The Potential for Renewable Energy Supply Chains

While Egypt has been eyeing electricity exports to Sudan, the Egypt-Sudan interconnection could also provide a means for Sudan to establish renewable energy supply chains to Egypt and beyond to Europe and the Middle East. Approximately 44% of Sudan’s total installed capacity for power generation comes from hydroelectric power,144 producing around 60% of its power.145 Solar power infrastructure is virtually nonexistent, providing about 0.18% of its electricity, while there is no installed capacity from wind power.146 However, the present state of solar and wind power in Sudan stands in stark contrast to the enormous potential of its resources. The deserts of Sudan’s northern and central regions receive similar levels of solar irradiation as Egypt’s Benban mega-solar power complex, while 50% of Sudan’s territory is suitable for wind power.147

Beyond electricity interconnection, green ammonia production for export or to power mining and manufacturing in Sudan are likely to incentivize foreign investment in solar and wind power infrastructure development. Sudan’s conditions are roughly parallel to those of Mauritania, in which companies from the UAE, Egypt, Germany, France and the UK have already invested in constructing green ammonia plants.148 One of the Mauritanian plants has already signed an MoU with the Port of Rotterdam for offtake of up to 600,000 tons of green hydrogen annually for sale in European markets.149 With its Red Sea ports, Sudan could similarly serve European markets as well as accessible Asian markets, although for now the ongoing civil war will remain a major deterrent to investment. As will be discussed below, the Amman-headquartered Iraqi firm Mass Group Holding (MGH) that operates a cement plant in Sudan is exploring the establishment of a green ammonia production plant in Jordan. A comparable facility could be established in Sudan to power cement production as well as for green ammonia exports.

Algeria and Tunisia: Challenges and Opportunities in the Central Maghreb

Despite its tremendous potential, Algeria’s renewable energy sector is woefully underdeveloped, accounting for just 0.8% of the country’s electricity generation in 2021.150 In 2022, Algeria’s installed capacity for power generation stood at 698 MW, comprised of 460 MW of solar power, 228 MW of hydroelectric power, and 10 MW of wind power.151 The 2030 target for Algeria’s Renewable Energy and Energy Efficiency Development Plan is 22 GW of installed renewable power generation capacity.152 Originally promulgated in 2011, the plan would require a thirtyfold increase in overall renewable capacity within six years, raising solar and wind power capacity to 15.58 GW and 5.01 GW respectively. The plan also designates 10 GW of the total renewable capacity for exports.153

Africa’s largest natural gas exporter, Algeria’s oil and gas sector accounts for 94% of its export revenues and dominates the economy.154 Like other industries outside the hydrocarbon sector, the development of Algeria’s solar power sector has been set back by institutional challenges that have hampered foreign private sector engagement.155 Renewable energy development could be incentivized in Algeria to reduce the carbon footprint of oil, gas, and petrochemicals production. In 2018, Eni and Sonatrach, Algeria’s state-owned energy company, built a 10 MW PV plant to support greenhouse gas capture in their Bir Rebaa North upstream oil and gas operations.156 Similar renewable power projects to “green” the fossil fuel industry seem likely and could potentially serve as part of the foundation for a green energy ecosystem.

In 2020, Italy’s Fimer, Algeria’s lead foreign partner in the realization of its 2030 renewable energy production goals,157 installed inverters for one of Algeria's showcase solar projects — the rooftop solar power system at Oran's Ahmed Ben Bella International Airport.158 Africa's largest rooftop PV installation, the 3.04 GW system will supply approximately 30% of the airport's electricity, helping to move toward its 2030 objective of installing 13.5 GW in PV production capacity.159 However, Algeria's flagship renewable energy project, the $3.6 billion, 4 GW Tafouk1 solar power complex, has floundered for lack of foreign investment, despite Algiers suspending its requirement to cap foreign stakeholders at 49%. Algeria could opt for numerous, small-scale independent power projects, an approach that has met with some initial success in neighboring Tunisia (see below).

Algeria’s development of a green energy ecosystem has been hampered by the country's general difficulties in developing a local manufacturing base, as evidenced by the inability of its nascent automotive sector and of its foreign partners to establish a reliable automotive manufacturing value chain locally.160 The country’s relatively successful iron and steel industry, with factories run by Qatari and Turkish firms,161 may be one of the most conducive industries outside the hydrocarbon sector for developing the use of renewable power, either directly or via green hydrogen.

In March 2023, Algeria unveiled its first hydrogen roadmap, which was developed with considerable assistance from the German development agency GIZ.162 However, the 30-year framework makes no commitments to specific types of hydrogen, making the roadmap consistent with Algeria’s desire to sell gray and blue hydrogen to Europe. Four months prior to the release of the roadmap in December 2022, Algeria signed a declaration of intent with Germany’s VNG, a subsidiary of German utility EnBW, to develop a pilot green ammonia plant. Although Germany’s KfW agreed to finance the 50 MW pilot green hydrogen facility,163 the agreement appears to have been a precursor to clearing a path for German purchases of Algerian natural gas. In early February 2024, VNG — formerly a major purchaser of Russian natural gas for German businesses — signed a landmark deal with Sonatrach to become the first German company to buy Algerian pipeline gas.164

While Algeria eyes capturing 10% of the European hydrogen market, the Ministry for Energy and Mines made clear the primacy of blue hydrogen in the short and medium term, declaring it an important step toward the development of green hydrogen.165 The greatest obstacle to green hydrogen development in Algeria may not be blue hydrogen but rather the insistence of Algeria and its European partners on transporting hydrogen via the existing natural gas pipeline network. The approach is being led by Italy, Germany, and Austria, which are seeking to create the “SoutH2 Corridor” that envisions using the undersea gas pipeline interconnection between Tunisia and Italy and Italy’s gas transmission system to transport hydrogen produced in the central Maghreb to Italy and central Europe.166 However, the technical and commercial viability of a trans-Mediterranean hydrogen pipeline is suspect and the project will likely either be highly climate unfriendly or economically infeasible if sufficient measures are taken to mitigate environmental damage and the release of greenhouse gases.167

When hydrogen is transported through undersea natural gas pipelines, the molecules severely degrade the hard steel. Unlike significantly larger natural gas molecules, the small hydrogen molecules can permeate the micro-fissures that develop in the pipe due to repeated changes of pressure,168 with the weld parts of the pipe even more susceptible to the formation and expansion of micro-fissures. While natural gas pipelines typically have a methane emission rate of 3.5%, the emission rate for the much smaller hydrogen molecules will be significantly higher.169 The released hydrogen would have a global warming potential 7.9 times that of the CO2 it is intended to replace.170

Aside from the pipeline material, the added compression costs to ship hydrogen through natural gas pipelines make the transmission of questionable commercial feasibility. Being 8.5 times less dense than natural gas, hydrogen is more difficult to move and therefore less energy efficient. For the same quantity of heat energy, hydrogen requires 200% more energy to compress than natural gas.171 The compressors in the existing natural gas pipeline network would need to be replaced with units three times as powerful, with three times the suction displacement, and with special capabilities to prevent the smaller hydrogen molecules from leaking.172 The capital expenditures and operating costs of transportation alone mean that replacing Algeria’s natural gas exports to Europe with hydrogen sent via pipeline would be over three times more expensive. 173

The proposal of transporting a blend of 20% hydrogen and 80% natural gas would not sufficiently resolve the transportation problems. Furthermore, even if green hydrogen were used, the blend would not be even “20% green.” The 80-20 proportion is by volume and contains only 86% of the energy content of the same amount of natural gas alone. The 80-20 blend requires 14% more of the blend to produce the same amount of energy as natural gas. Therefore, the greenhouse gas reduction of a blend with 20% green hydrogen would be closer to 6% or even less when accounting for the fact that the 80-20 blend would require 13% more energy to compress.174

The extent to which Algeria and its international partners succeed in the attempt to ship green hydrogen via undersea pipelines will determine the fate of Algeria’s green hydrogen industry, unless Algiers and its European partners can be convinced to opt for green ammonia. In the absence of green hydrogen or the manufacture of export products in Algeria powered by renewable energy, trans-Mediterranean electricity interconnection via Tunisia will be Algeria’s only export offtake option for its renewable energy production.

In 2022, Tunisia possessed 472 MW of installed power generation capacity from renewable sources, accounting for 8% of its total.175 Wind power accounted for the largest amount of renewable capacity with 244 MW, while solar power stood at 166 MW and hydroelectric power at 62 MW. In the same year Tunisia revised its 2030 target upwards from renewable power comprising 30% of total power generation capacity to 35%, as an intermediate step toward reaching 80% by 2050.176 Representing an almost 900% increase in renewable power capacity, the immediate focus of the Tunisian government is finding foreign companies to build a large number of small renewable facilities as independent power projects, with an emphasis on PV solar power. In 2023, Tunisia initiated tender offerings for 18 projects with a combined capacity of 1.7 GW — ten 100 MW solar power projects and eight 75 MW wind power projects.177 Given Tunisia’s comparatively small population, these projects collectively could have some export offtake potential. By themselves, they are insufficient to create a green energy ecosystem or international renewable energy supply chains, but they could provide a vital foundation for the development of both.

Tunisia’s recent efforts to expand its renewable capacity are built upon the government’s push to revise the legal framework to attract foreign direct investment (FDI) in the development of renewable energy infrastructure.178 The success of the new concessions regime to encourage the completion of these projects and the network of partnerships with foreign companies that emerge from that success will determine whether Tunisia will realize its renewable energy potential. The initial results offer some cause for optimism. In 2023, the UAE-headquartered renewable energy developer AMEA Power reached its final close on a 120 MW solar power plant in Tunisia’s Kairouan governate.179 Winning the project in December 2019 in a previous tender program launched by Tunis, the government signed the concession agreement and power purchase agreement in June 2021 under the new concessions regime for projects over 10 MW.180 Financed by the International Finance Corporation and the African Development Bank, the Kairouan Solar Plant is the first solar project to reach financial close under the new concessions regime.

To further enhance the effectiveness of Tunisia’s new concessions regime, the government will need to overhaul the fiscal health and transparent functioning of the state-owned energy production and distribution company STEG (Société tunisienne de l'électricité et du gaz), which oversees the development of offtake mechanisms that will be vital to Tunisia’s formation of international renewable energy supply chains, both via green hydrogen and electricity interconnection. How Tunis engages international financial institutions to help achieve accountability in bills payment and a workable balance of tariffs, revenue requirements, and subsidies will greatly impact the country’s success going forward.181

Tunisia’s National Green Hydrogen Strategy aims to produce 8.3 million tons of green hydrogen, 6 million of which are slated for export.182 Although Tunisia has strong potential for green hydrogen production, the limited efforts to develop the sector have occurred within a development aid framework. Both the SoutH2 Corridor project and green ammonia development are hampered by this limitation. The concept of the SoutH2 Corridor builds on a 2021 study published by GIZ assessing the potential of Tunisia’s hydrogen industry that did not address the previously discussed challenges involved in transmitting hydrogen through undersea natural gas pipelines.183 Spearheading Tunisia’s green hydrogen program is TuNur, a joint venture between Tunisian investment group Top Group and UK-based firm Nur Energie, which came to prominence through the endorsement of the Desertec project.184

Green ammonia development in Tunisia was kickstarted in December 2020, when Tunisia received a $36 million development grant from Germany for the construction of a pilot green hydrogen project now known as H2 Vert.185 Officially launched in June 2022, the small-scale plant is slated to produce 1,500 tons of green ammonia per year, with GIZ designated to oversee project implementation.186 The economic logic for Tunisia to develop a green ammonia industry linked to fertilizer production, along lines similar to Morocco’s engagement with foreign private sector investors, is more compelling. Faced with similar agri-food production problems as Egypt, Tunisia can only satisfy 25% of its domestic fertilizer demand.187 Replacing imported gray ammonia with locally produced green ammonia would boost Tunisia’s domestic fertilizer industry. With a total population three times smaller than that of Morocco, Tunisia would be well-positioned to develop an export industry for surplus green ammonia or possibly higher-value fertilizer, given the supply shortages in Europe and Africa.

As in the rest of North Africa, water scarcity poses a significant challenge for green hydrogen production in Tunisia, where about 80% of the diminishing water resources are used for agriculture.188 Plagued by drought, Tunisia’s situation has been exacerbated by the poor stewardship of its scant water resources.189 The food and water problems are not insurmountable and their amelioration could be accelerated by the development of a green ammonia industry if sufficient desalination plants and the renewable energy infrastructure to power them are constructed. Green ammonia exports could incentivize the significant foreign investment required to achieve these solutions, as has occurred with the development of large-scale green ammonia production in Mauritania.190 The success of the most recent tenders for solar and wind power under Tunisia’s new concessions regime could form an avenue for attracting foreign private sector partners for Tunisia’s green ammonia development. An opportunity exists for Morocco, Egypt, and Arab Gulf hydrogen actors to cooperate with Tunisia as well. The opportunity is enhanced by the fact that green ammonia is traded via seaborne exports and would not require overland pipeline or electricity interconnection transit over Algerian or Libyan territory.

Beyond green ammonia and fertilizer exports, Tunisia’s automotive components industry could support the development of an international renewable energy supply chain, if the manufacturing processes were powered by renewable energy. Tunisia’s automotive parts sector accounts for about 14% of its exports and employs over 90,000 Tunisians.191 With top export markets being Germany, France, Romania, and Italy, Tunisian automotive components manufactured using renewable power would establish an import Tunisia-to-Europe renewable energy supply chain.192 Tunisia’s flagship company, the automotive wire and cable manufacturer Coficab, is an industry leader, positioning the company at the forefront of automotive electrical system supply chains for EV production. Coficab operates a factory in Morocco to supply its auto manufacturing ecosystem, creating an opportunity for synergy with the neighboring state in creating an industrial renewable energy supply chain.

Trans-Mediterranean interconnection forms an important offtake mechanism for Tunisia, which is partnering with Italy to interconnect their electricity grids via a 192-km-long, 600 MW undersea cable between Tunisia and Sicily.193 Known as the ElMed interconnector, the project was scheduled for completion in 2025, but now is on track to be completed in 2028 thanks to the financial infusions of €308 million and $268 million respectively by the European Commission in December 2022 and the World Bank in June 2023.194 In contrast to Morocco’s interconnections with Spain and Portugal, Tunisia’s interconnection with Italy will enable power exports to the wider EU electricity market.

Arabian Peninsula

The Arabian Peninsula has long been a leading production center for the oil and natural gas traded on global markets. Among the countries on the peninsula that form the membership of the Gulf Cooperation Council (GCC) are the world’s leading oil and natural gas producers with almost 100 years of experience as hydrocarbon fuel exporters. At the same time, these countries possess solar energy resources almost at the same level as the nations of North Africa. Shaped by their experience in international hydrocarbon value chains, most of the GCC states have placed international renewable energy supply chains at the forefront of their respective approaches to developing their own renewable power infrastructure for a post-hydrocarbon age.

At the same time, several of the GCC nations are using the energy transition as an opportunity to diversify their economies by developing 21st century, climate-smart industrial manufacturing and agri-food production. The UAE has been at the forefront of developing a green energy ecosystem, while Saudi Arabia is seeking to emulate the Emirati approach in a manner appropriate to its own needs and often on a grander scale. Global LNG giant Qatar is charting its own similar course while Oman aspires to use the opportunity to expand its international footprint. Especially in the case of the UAE and Saudi Arabia, the two countries are using their experience and capital to become an engine driving the development of renewable energy infrastructure and green energy ecosystems in Europe, Asia, and Africa as well as in their own countries. These efforts are placing the Arabian Peninsula at the center of an emerging pattern of renewable energy supply chains.

UAE: A Green Energy Ecosystem as an Emerging Hub for Renewable Energy Supply Chains

The UAE is home to one of the MENA region’s most rapidly developing green energy ecosystems. A signatory to the 2015 Paris Climate Accord and committed to achieve net zero by 2050, the UAE has been investing extensively in energy transition, both at home and abroad, since it ratified the Kyoto Protocol in 2005. The UAE’s cumulative investment in clean energy projects from 2005 to 2023 totals over $40 billion.195 Beyond its borders, the UAE has invested in renewable energy projects across 70 countries worth a total of $16.8 billion.196 These extensive foreign investments reflect the Emirati approach, which regards its own green energy ecosystem as a central connectivity node in a nexus of international green energy ecosystems. With this outlook, the UAE has been positioning itself to become a hub for inter-regional, renewable energy supply chains.

The UAE is accelerating its development of power generation from renewable energy, a process that in the short term frees up natural gas for industrial use and export to help maintain favorable foreign trade balances and robust GDP growth while the country implements its energy transition. The UAE’s forward-leaning policies have succeeded in making it home to the largest renewable energy power generation capacity in the Arab Middle East. In 2022, the UAE boasted installed solar power capacity of 3.04 GW, accounting for over 99% of the Emirates’ renewable energy capacity.197 In July 2023, the UAE announced its updated National Energy Strategy to achieve in 2050 an energy mix of 44% renewable energy, 38% natural gas, 12% “clean coal,” and 6% nuclear energy.198 With the interim goal of tripling the share of “clean energy” in its power mix by 2030 to 30%, the UAE is embarking on $54.5 billion in renewable energy investments.199 By 2030, UAE is aiming to achieve a 19.8 GW “clean energy” power generation capacity,200 including 14.2 GW of renewable energy, quadrupling its 2022 renewable energy capacity.201 Most of the 14.2 GW will come from the expansion of the UAE’s solar energy capacity, with a combined 470 MW coming from waste-to-energy and pumped-storage hydropower.202

The Emirati efforts to develop its green energy ecosystem have benefited from the skillful leveraging of the country’s experience in oil, natural gas, and petrochemicals production and export, encouraging collaboration between its national oil companies, firms engaged in renewable energy development such as Masdar (Abu Dhabi Future Energy Company), and the country’s various power authorities. This collaboration has been facilitated by the bureaucratic integration of state-owned enterprises across the country’s seven emirates. In 2018, the UAE’s four power authorities — the Abu Dhabi Water and Electricity Authority (ADWEA), the Dubai Electricity and Water Authority (DEWA), the Sharjah Electricity and Water Authority (SEWA), and Etihad Water and Electricity (EWE), which supplies electricity in Fujairah, Ras al-Khaimah, Ajman, and Umm al-Quwain — were integrated into the then newly created national Ministry of Energy and Infrastructure.203 The consolidation served to streamline strategic planning by bringing state-owned energy companies into a national framework. For example, the integration of ADWEA saw the Abu Dhabi National Energy Company (TAQA) — 74.1% of which was owned by ADWEA — and ADWEA’s then 10 power and water desalination plants come under the new ministry’s authority.204